Northwest Co-op. These are post 1968 riot affordable housing units. The bay window like sections that jut out on the 2nd floor reference the circa 1900 Bates Street houses with a similar type (but less boxy) window.

They are not public housing. They might accept Section 8, but it is not public housing.

I’m trying to clean up a bunch of papers I have. I hope I can be brave enough to toss them into the recycling bin. One piece of paper is something I got from the Washington Post archives via ProQuest.

Fine Home At Low Rent: Bates Street Buildings Erected for Wage Earners, Are Up to Date: Sanitation Was One of Chief Aims of Washington Company Which Has Erected Them, is an article from July 25, 1915 on page RE5. The short of it is an article about the Washington Sanitary Improvement Company (WSIC) having built homes for unskilled laborers, the workforce housing of 100 years ago.

The paper sells the WSIC as a good investment providing housing $10 for 3 rooms and a bath and $12 a month for 4 rooms and a bath. There are other units to rented at $7.50 and $8.50 a month for two rooms and a bath. These homes are on Bates Street NW.

Because of copyright, I’m not providing a copy here, but you can access the article via the DC Public Library. You will need your DC Library card to use this resource.

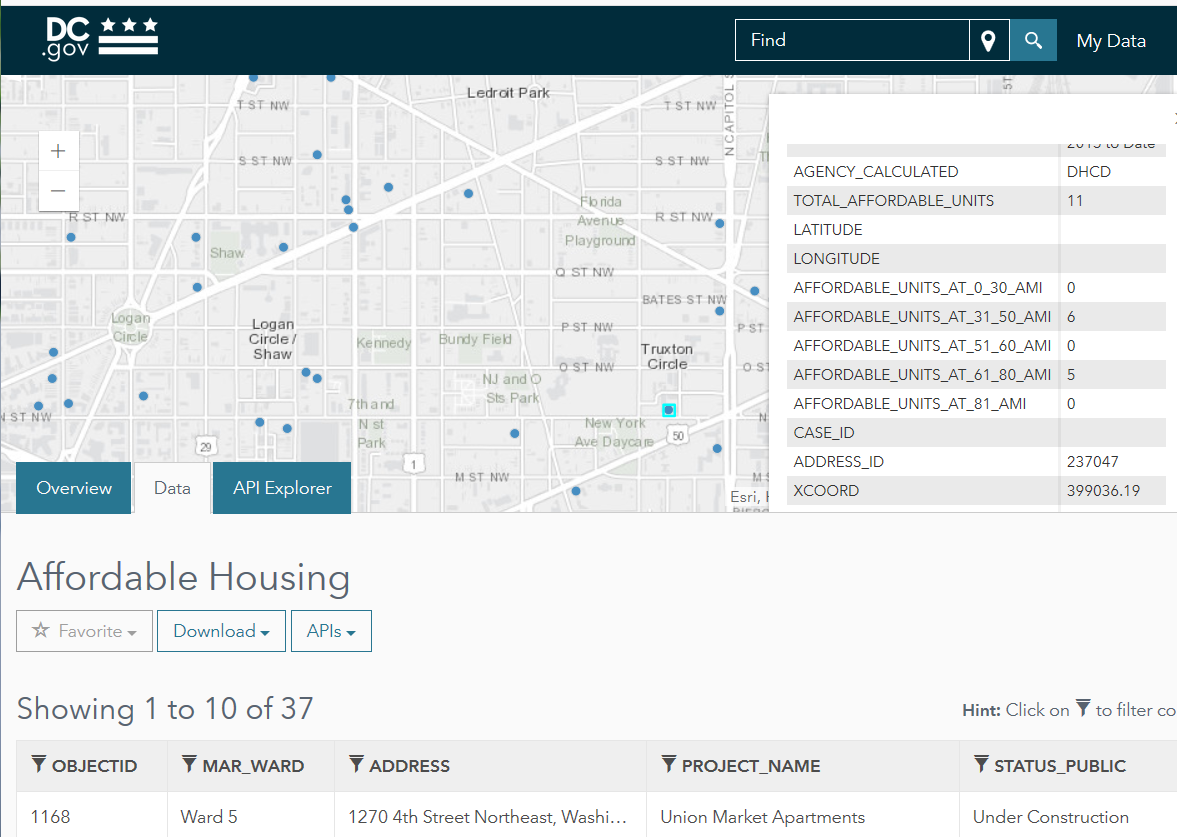

Screen Capture of http://opendata.dc.gov/ data set of Affordable Housing

I started searching because the Open Data DC.gov site has a map so you can find affordable housing projects in the District. So I went to the side and drilled down to Truxton Circle.

So I saw Chapman Stables was in there and there are supposed to be 11 affordable unit of the 100 plus units. Six units are at 31%-50% AMI and 5 units at 61%-80% AMI.

But then I wondered. Wait. Condos have condo fees. These fees can start off reasonable and then if something happens creep or jump up. Then I wondered what do these affordable units look like? Are they segregated from the other units, like some apartment buildings?

So I went a looking at the DC property sales database to look at what sold below the $300K advertized basement price. This is public information, but I’m not going to use names or unit numbers. I found 5 units, they are not all on the same level, and they are not all studios. The first was sold on October 9th for $237,400 is a corner two bedroom unit. I noticed several of these affordable units share a wall with some common space things, like stairwells. Three units were sold for $114,600 in 2018. Two of those are one bedrooms and one is a studio. The one bedrooms share a wall with a common space thing and the studio is well, a studio. And lastly a one bedroom unit sold for $214,300.00 on October 16, 2018, and it only shares walls with other units.

The monthly condo fee for a one bedroom is $362. The fee for a typical studio is less than $300, and for a two bedroom in the $600 range. Remember kids, the condo fee is in addition to the mortgage and real estate taxes. I don’t know if the buyers of the affordable units get to pay a reduced fee or must pay the same rate as the market rate buyers, because everyone must contribute to the maintenance, trash, and all that other good stuff.

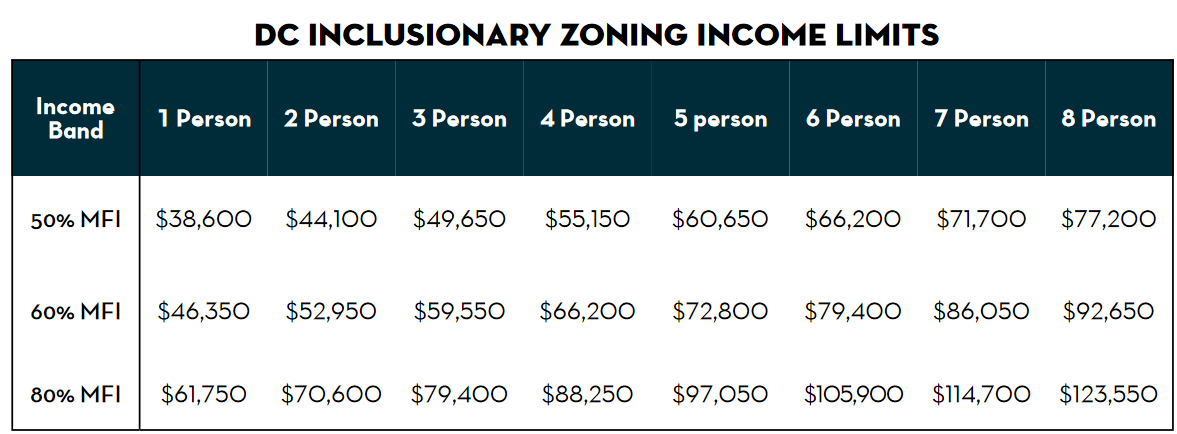

Also, let’s look at the categories of 31% to 50% AMI and 61% to 80% AMI. This is more about the buyer of the unit than the unit. Six units are for 31-50% AMI. According to the Department of Housing and Community Development’s chart that’s an income ceiling of $41,000 for a single person and $46,900 for a household of two. On the off chance the two bedroom was available for this category, a household of four’s limit is $58,600. There is nothing for the 51-60% AMI group. Five units were set aside for the 61-80% AMI group and the ceilings are $65,650, $75,000, $84,400 and $93,750 for households of one, two, three and four persons.

There is another condo in Truxton that is not yet completed, which has just 2 affordable units for 61-80% AMI, and that is Compass’ Five Points Flats. I have no clue as to what the condo fees for this thing will be.

It is easy for me to imagine single teachers, non-profit workers, civil servants, or savvy retirees, being able to fit into these income categories AND keep up with the HOA/condo fees. What I cannot see is how people who are in those AMI groups find out the availability and price of these units. As I see with Chapman Stables, they did manage to find those units.

When I read studies about housing, housing stock and affordable housing, as it applies to areas like Shaw, I can’t help feeling there is a very wrong assumption flowing through them all. I encountered, that feeling when talking to a renter on my street who would love to buy, but was unaware of what some of us did to make affordable homes livable, and once they became livable, unaffordable to people like him. A house that was affordable in Shaw in the 80s or 90s is probably not the same house that stands today.

In the 1940s-50s Shaw was described as a slum. A slum was defined in some writings as an area where a significant number of houses lacked indoor plumbing or interior toilets, thus slummy Shaw. I want you, dear reader, to think about that. Living somewhere, when you have to go, you’ve got to go….. outside. But now there are laws and regulations so when you rent a place, you get that fancy pants indoor bathroom with hot water.

But there are other housing deficiencies that houses in the 90s and early 00s suffered from because of the history of disinvestment in the neighborhood. Disinvestment meaning, landlords and homeowners had no incentive to maintain properties, beyond necessity, with little to no equity gained. Not updating kitchens, or electrical wiring, or plumbing, resulting in cramped little kitchens, wiring that would fry your electronics, and leaky pipes.

House under renovation.

Then came the renovations and the gentrification. Some were crappy and cosmetic, like my house when I bought it, and some actually fixed long neglected problems or updated systems. Even crappy renovations cost money and those costs are pushed onto the end user, the home buyer or the renter. Yes, there are places where there has been no, to little reinvestment, and the prices act as if there were.

So next time you read a report that assumes the equity gained due to gentrification is unearned, question if the house that was affordable in year X is of the same quality, with the same features, when it is unaffordable in year Y.

The Advoc8te who runs Congress Heights on the Rise pointed out a problem with income limited or affordable housing in DC. That has continue to bug me, because for years at community meetings when ‘workforce’ housing is trotted out residents are told it would allow government workers such as police and teachers to live in the communities they serve. Then when I see the income limits and then look at the starting salaries for DC police and teachers, I think, I’ve been lied to. I decided to just glance at what DC pays its teachers and police. Almost all government employees’ salaries are public, mine, my spouse’s, my cousin who makes a quarter of a million, it’s no secret, so I can actually see what DC pays. Grade school teachers, not teachers aides, not substitute teachers, nor administrative staff, if they’ve been teaching 3-4 years at least, are in the $60-70K range. There is a school librarian making six figures, as a fellow librarian, I say good for them. I didn’t pay much attention to MPD salaries, but officers are making over $60K. That makes sense if this poster is true and the pay starts at $55,362. If a teacher and cop fall in love, a la rom-com adventure, they’re making six figures as one household if they marry.

Okay, let’s get back to housing and income limits. There are a couple of key things you have to keep in mind, household size and AMI, area median income or MFI, median family income.

Say Anna works for a non-profit and makes $40K, and there is a new affordable housing development with studios and 1 bedrooms that’s at 50% and 60% AMI/MFI. She might be able to get a studio at 60% MFI, but not at 50%. She makes too much at 50%. But if Anna was a single mom, a household of 2, aiming for a 1 bedroom (I don’t remember the rules about this), she would qualify at 50%. Looking at this table, and going on my memory, the DC government employees who could qualify are school custodians, teacher’s aides, and some DC Public Library staff. The city doesn’t pay our librarians enough.

If you haven’t read Congress Heights on the Rise’s (CHotR) blog, please do. The author, Ms. Peele is telling some serious truths about the problem of affordable housing in her neighborhood. It is not the same problem of affordable housing experienced in NW, the problem is there is a little too much affordable housing and not enough market housing.

One of the post’s “Why investing ONLY in income-capped housing in Ward 8 is setting us up for failure,” can be summed up as affordable housing needs to be spread around more equally across all 8 wards and not concentrated East of the River (EotR). She points out that the majority of the available apartments for rent in her area are income capped, which means a single person making $51,000 cannot rent an apartment there, and forget about a married couple. Without those sort of renters, that middle class contingent, the urban amenities that make DC fun are in short supply in her neighborhood, and she has to drive elsewhere for fitness and food.

Continuing in another post “MORE OF THE SAME: 7 more income-capped housing projects planned for Ward 8,” she is obviously frustrated with the DC government’s (DHCD) housing policy of more income capped housing. This sort of policy keeps out the kind of residents who could support the businesses (and jobs) she wants and provide the kind of role models kids in the neighborhood need. The income limits keeps out nurses, police officers, teachers, and most other professionals. Many of the income limit apartment buildings are at 50% MFI/AMI (Median Family Income/ Area Median Income) so a single person cannot make more than $41,050. The starting salary for a DCPS teacher is supposed to be $55, 209, and the starting salary for a MPD police officer is $55,362. It would have to be at 80% MFI/AMI for a single income teacher or police officer. Logically, if you had a married couple (the cop married to a teacher) they would blow past the $46,900 50% MFI/ $76,000 80% MFI limits for a household of two, and three.

Aren’t we just repeating the mistakes of the past with new packaging? Concentrating poverty is destructive, cruel and wrong. We, as a city, have done it before with public housing and created environments of unemployment, crime, death and dysfunction.

So I was bopping around the YouTubies as I normally do and decided after the question of what foods are great for baby led weaning, I decided to ask, what is affordable housing. I know what is affordable housing, well its technical definition for DC. But what does it mean in real life for tenants?

Although not for DC (New York City, different animal) I came across this from a fitness Youtuber Imani Shakir.

I love how she talks about her experience with the system and how it works there. Just going by her video this is what I learned: You need an on-line housing profile; don’t apply for everything, just apply to the buildings where you qualify; Your chances are better if you pick a building in your area; You need to respond quickly and have accurate contact info; You may need letters from your current and former bosses in addition to pay stubs as some of your application documentation when asked. You might have less than 2 weeks to get those documents together; and the biggest take away, it may take years to get an affordable unit. In her case it was 3 years.

We normally hear about affordable housing from politicians, activists, and administrators, but almost never from recent applicants and recipients of affordable housing.

“Affordable Housing” gets thrown around a lot in DC, as in there isn’t too much of it. HUD (Housing & Urban Development) defines affordable housing as, “In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income for gross housing costs, including utilities. Please note that some jurisdictions may define affordable housing based on other, locally determined criteria, and that this definition is intended solely as an approximate guideline or general rule of thumb.” Unfortunately for me, DHCD (Dept of Housing and Community Development) doesn’t have such a nice glossary, or at least one that I could find, and as HUD hinted, the locality may have other criteria.

What DHCD does somewhat define are Affordable Dwelling Units (ADU). According to the website, “Affordable Dwelling Unit (ADU) is an umbrella term applied to for-sale and for-rent homes that are locally restricted for occupancy by households whose income falls within a certain range. ADUs are generally offered at a below-market rate. The DC Department of Housing and Community Development (DHCD) monitors and enforces compliance with ADU requirements in the District of Columbia.” The income ranges depend on size of household, not makeup (ex. a 2 person household could be 2 adults, or 1 adult and child).

The 2017 income limits and ranges and all that can be seen in a PDF at this link. If affordable housing or a proposal for affordable housing is the subject of an upcoming community meeting in your neighborhood, print out the latest on affordable housing income limits and bring it to the meeting. Typically when I bother to ask the developer or whomever the representative is for some proposed project about income, they are unsure what the limits are. They do know that they are supposed to have X number of units out of Y number of units at 50% or 30%. Sometimes they mention how many bedrooms per unit and let’s say no one is building units for large families.

I feel I need to also define ‘public housing’ as I tend to see comments on DC related blogs and sites referring to a housing complex taking vouchers (sometimes called Section 8) as public housing. The Northwest Cooperatives for the 10 zillionth time are not public housing. Why do I have a picture of the NW Co-op? It is affordable housing as they do take section 8 vouchers and the housing was built with the help of HUD subsidies. The DC Housing Authority has 56 public housing properties it maintains and you can see that list here. If it isn’t on that list, it’s not public housing.

There are a handful million dolla properties for sale in Truxton Circle, so we’re not affordable no more. And this place gentrified some time ago, so stick a fork in that. Yes, the Northwest Cooperative is still an affordable place and there are a few (a few) ‘affordable’ units in the pipeline for the vacant lots. I suspect it’s not easy to just get a rental at the Co-op, and there will probably be some competition for the new units. As far as something “affordable” to buy, you’re stuck with either condo units or handyman specials. Chapman Stables has two units under $400K, one being a studio the other a 1 bedroom. There’s a 1 bedroom in a smaller condo on Q St for $375K. Townhouses in that general price range are handyman specials already under contract. There is a house on my block that is on the market that requires some work to make livable and would be an okay purchase if there are no plans for an expansion.

Personally, I’m not a fan of condos, as they come with condo boards, which sometimes contain crazy people. However, a condo is like a starter home. It’s not the best place to build equity, but it’s something. A person can move up from a condo to a house.

But some say it is impossible to come up with the 20% down payment to buy a place. I’m going to tell you a little secret. You don’t need 20%. Twenty percent is very nice, it makes your mortgage payments cheaper, but it isn’t required. I know this because I did not have 20% or even 10% when I bought my house. I think I put down 3%. There are down payment assistance programs in DC to help. Well, what about people who can’t even save 3%? Houses and condos have problems, even new ones, and those problems cost money. If one cannot keep money in savings, as soon as one of these problems crop up, homeownership will sink the owner.

So the Post has an article about middle class incomes rising and mentioned the national median income for 2016 was $59,039. Keep in mind that is for a household, this will become important later.

The median income for the DC Metro area is way higher. Twice as high, at $110,300 for 2017 according to HUD. You might be thinking, I don’t make that much, who the hell is making that money? Well remember this is for households, those incomes are typically for a four person household. This may be two working adults and two kids, or one extremely well paid working adult and 3 dependents.

If you’re a singleton, the AMI is $77,300, pat yourself on the back you are definitely middle class in DC. If you’re single in DC making $52,550 or less you are low income (80% AMI). An annual income of $38,650 or less, you are very low income (50% AMI) and $23,200, you’re poor (extremely low income). I will leave it to you to decide if at 80% AMI (Area Median Income) you are middle class or not.

Using the Federal government’s salary table the good news is for the DC-Baltimore area there are no full time poor workers. Same thing for MPD police who are in the union, the base salary for a Class 1 officer (2015) is $53,750. That puts them in the 80% AMI region if they have 1 dependent. A starting teacher for DCPS with just a BA should get $51,359 annually. So when someone promoting workforce housing proposes having income limits at the very low income level (50% AMI) and says it’s for teachers and police officers, they are full of $hit. Even a family of four would make too much at the 50% level after the lowliest teacher’s 5th year or for a teacher with a MA 2nd year of service and a cop’s second year, assuming their spouse (if any) wasn’t working.

Being in the 80% AMI range can be a pretty sweet spot. Just before I bought my house I was below the 80% AMI and was able to qualify for a bunch of housing programs. There was a property tax abatement I qualified for that lasted about 5 years until I made just a smidge too much and the low interest rate mortgage from DCHFA. Neighbors at the 80% AMI are the kind of people you want. If they are young it is only a few years before they are at or above the AMI.